See also

10.06.2026 11:56 AM

10.06.2026 11:56 AMLast week was relatively quiet in terms of New Zealand macroeconomic data. Following the Reserve Bank of New Zealand (RBNZ) meeting, no significant new information emerged, and market attention is now focused on the upcoming first-quarter GDP report.

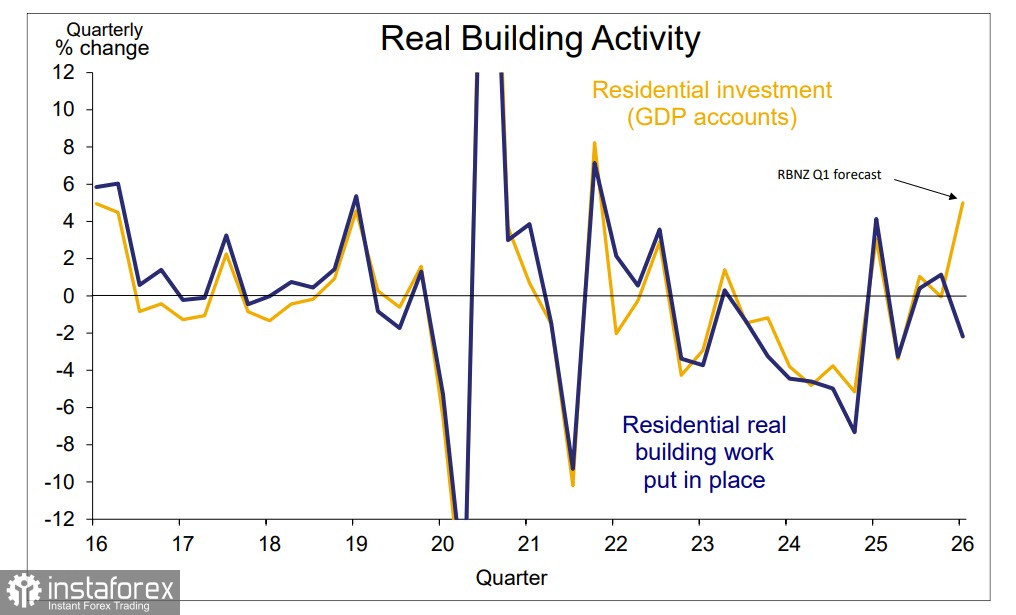

Overall, New Zealand's key economic indicators, such as retail sales and international trade, continue to show stability. However, first-quarter construction sector data released last week altered the overall picture. A significant 3.5% quarter-on-quarter decline in real construction activity came as a surprise and contradicted expectations of substantial growth.

As a result, BNZ revised its first-quarter GDP forecast lower to 0.7% quarter-on-quarter from the previous estimate of 0.9%. There is a risk of further downward revisions if the upcoming manufacturing, wholesale trade, and services sector data fail to show positive momentum.

Against this backdrop, the sharp increase in residential building permits issued in April stands out. The figure rose by 10.9% month-on-month and by an impressive 52.7% year-on-year. This result was an unexpected positive surprise and contrasted sharply with the data on completed construction activity.

It is worth recalling that the latest RBNZ meeting revealed divisions among Monetary Policy Committee members, with three of the seven members voting in favor of a rate hike. The market is currently pricing in a high probability of three interest rate increases before the end of the year. Therefore, the GDP data may either reinforce these expectations and support the New Zealand dollar (kiwi) or, conversely, strengthen negative sentiment.

Today's key event will be the release of the U.S. inflation report for May. Forecasts point to an increase in headline inflation from 3.8% to 4.2% and in core inflation from 2.8% to 2.9%. If these expectations are confirmed, it would provide additional support for U.S. dollar buyers.

However, there is an important nuance. The yield on 5-year Treasury Inflation-Protected Securities (TIPS) has been declining steadily and has reached a three-month low. This may indicate that businesses do not expect inflation to accelerate as significantly as current forecasts suggest. If this assumption proves correct, the U.S. dollar could weaken substantially by the end of the day, creating room for a corrective advance in the New Zealand dollar. For now, this remains a hypothesis, but one that has a reasonable basis.

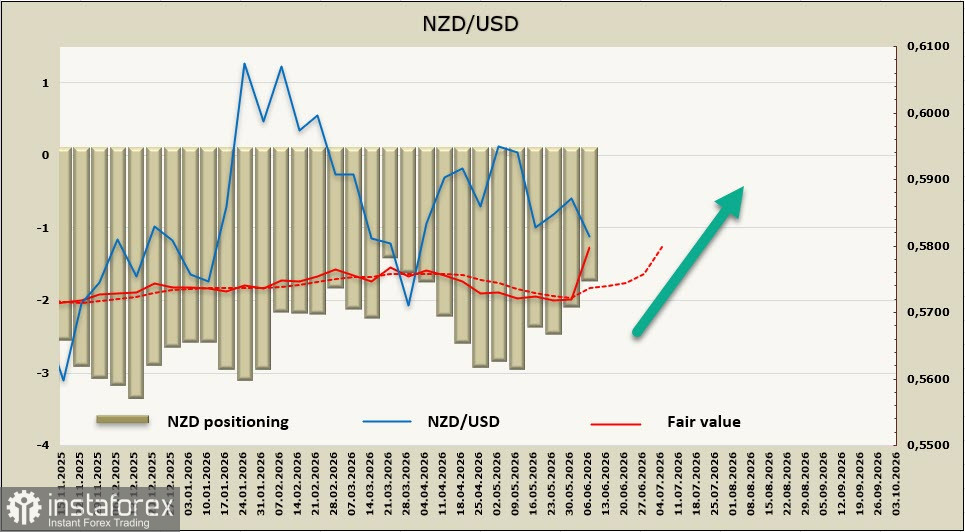

The net short position in the NZD decreased by $321 million during the reporting week to -$1.67 billion. At the same time, the estimated fair value unexpectedly turned higher, increasing the likelihood of a corrective rise in NZD/USD.

A week ago, we identified the 0.5780–0.5790 level as a target, and that objective has been achieved. As of Wednesday morning, we believe the probability of an upward correction has increased. The kiwi may still decline further toward 0.5676 after making a second attempt to break below support at 0.5780–0.5790. However, considering the behavior of the estimated fair value, we believe a move toward the midpoint of the sideways range that has contained the pair since early April is more likely. In this regard, the 0.5870–0.5890 resistance zone may serve as a potential upward target. Fundamental reasons for a sustained rally remain limited, but the probability of such a corrective rebound has increased noticeably.