यह भी देखें

10.12.2025 04:48 AM

10.12.2025 04:48 AM

The market is formally preparing for the standard scenario. The Federal Reserve is likely to cut interest rates by 0.25%, and the rhetoric will shift to a moderately dovish stance looking ahead to 2026. While tariffs have a moderate impact on inflation, the employment segment is losing momentum much faster. The hiring rate is slowing, layoffs are not increasing, and unemployment is rising. Logically, a weak labor market pushes the central bank toward further easing.

But the real intrigue lies elsewhere. The situation with the repo system and the reduction of bank reserves heightened money market volatility in November. Authorities face the risk of a temporary liquidity failure. To stabilize the situation, the Fed will almost certainly announce a program to purchase short-term securities with a potential volume of around $40 billion monthly starting in January. This effectively represents a soft form of quantitative easing (QE), albeit disguised as technical balancing.

There is also a political factor that the market seems to underestimate. The appointment of Kevin Hassett as the future head of the Fed will change the trajectory of expectations even now. Formally, Jerome Powell will be at the helm for three more meetings, but investors will closely monitor signals from the prospective new head of the U.S. central bank. He is known as an advocate for loose policy, and his position is closely tied to the White House. This implies an increase in the risk premium on long-term rates, particularly given the ongoing inflationary pressures. Essentially, with his arrival, a gradual political rethinking of the monetary policy direction will begin, especially as we approach the midterm elections in 2026.

This will be a key factor for all classes of risk assets. The bond market faces an additional challenge. Over the next four months, the U.S. Treasury must issue around $0.5 trillion in new bonds. Therefore, even if the rate decision tomorrow brings no surprises, the strategic implications of the meeting appear more serious:

The December FOMC meeting is becoming one of the most atypical in recent years. The central bank is approaching the final decision of the year essentially without key macroeconomic benchmarks. The six-week pause in federal government activity has blocked the publication of employment and inflation reports. As a result, the December 10 meeting takes place without official data since September, sharply increasing uncertainty and complicating the assessment of the current cycle.

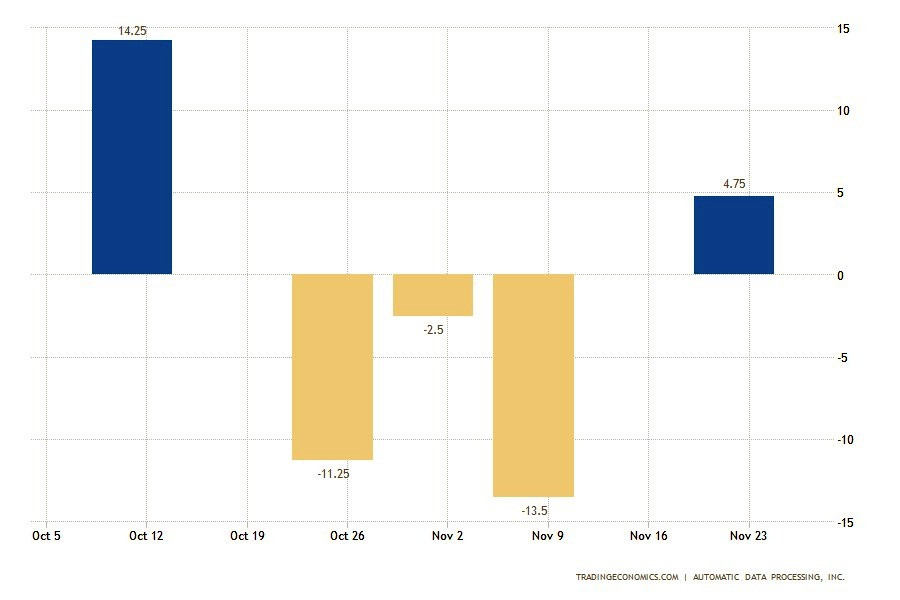

The number of voluntary resignations has fallen to 2.94 million — the lowest level since 2020. This reduction affected sectors such as accommodation and food services, healthcare and social assistance, and federal government jobs. Meanwhile, layoffs rose in the entertainment, arts, and media sectors. The proportion of workers leaving voluntarily has dropped to 1.8%, reflecting employees' weakened confidence in the labor market's stability.

The vacancy situation appears more stable. In October, the number of job openings increased to 7.67 million with moderate positive dynamics in retail, transportation, and utilities. On the other hand, parts of professional services have seen a decrease in demand for personnel. The overall configuration of the market indicates gradual cooling rather than a sharp decline.

This gap between private and official indicators makes the rate decision extremely challenging. The Fed currently faces a high risk of error on both sides: from excessive tightening to excessive easing. The absence of official data on inflation and employment since September has put the Fed in a situation where its two key tasks—price stability and maximum employment—are in direct conflict:

In the absence of fresh data, the December meeting becomes a balancing act between opposing risks.

And a consensus does not imply unity. Despite the complex backdrop, the market almost unanimously prices in a 0.25% rate cut. This step is seen as limited insurance: it reduces the risk of a sharp deterioration in employment but does not change the parameters of the fight against high inflation. However, internal divisions within the Committee may become significant. Analysts expect more "against" votes. Such a result would be perceived as a signal of weakening Powell's influence and growing fragmentation within the FOMC, complicating the formation of expectations for 2026.

The intrigue of the meeting lies not only in the scale of the current rate cut. The market is focused on the dot plot update, which shows policymakers' individual forecasts for the path of the federal funds rate in 2026. Currently, the market expects four rate cuts next year. This suggests support for assets and creates a bullish scenario for the stock market. However, the more stringent option appears to be more likely. If the median dot reflects only two rate cuts in 2026, this would signify hawkish easing:

The upcoming Fed decision takes on significant political dimensions. President Trump openly supports rate cuts as a tool to counter potential inflationary effects of his tariff policy. Against this backdrop, the Fed Chair must maintain an image of independence and avoid politically motivated decisions. Thus, overly aggressive easing may be interpreted as an attempt to support a future administration or yield to external pressure. Maintaining a tough stance, on the contrary, would risk accusations of hindering economic transition.

Amid these expectations for the Fed's decision, attention has turned to Trump's comments made in an interview with Politico. He noted that he might adjust specific tariffs to lower consumer prices and claims that he has already made such adjustments in several categories. "Prices are all falling. Everything is declining," said the U.S. President, adding uncertainty to the assessment of future inflation dynamics.

The current configuration indicates a moderate risk appetite, but it has not yet led to the formation of directional positions. Ahead of the Fed meeting, market participants are avoiding significant decisions. The rate statement and the press conference on Wednesday will be key sources of signals regarding the future course of U.S. monetary policy. Powell's comments and responses to questions could provide deeper insight into the Fed's leadership stance. The market will also receive updates on economic forecasts and the dot plot, which reflect the outlook for the economy next year.

Furthermore, this meeting will be the last for the current voting members. New representatives from Cleveland, Minneapolis, Dallas, and Philadelphia will replace those from Boston, Chicago, St. Louis, and Kansas City. The situation is further complicated by active discussions about replacing Powell. All of this creates tension among investors, and therefore, a lack of positivity in the currency and bond markets has been observed recently. Moreover, Bank of America strategist Michael Hartnett warns that the start of the Santa Claus rally may be at risk. Although a rate cut would support stocks on Wall Street, investors are counting on a comprehensive set of factors:

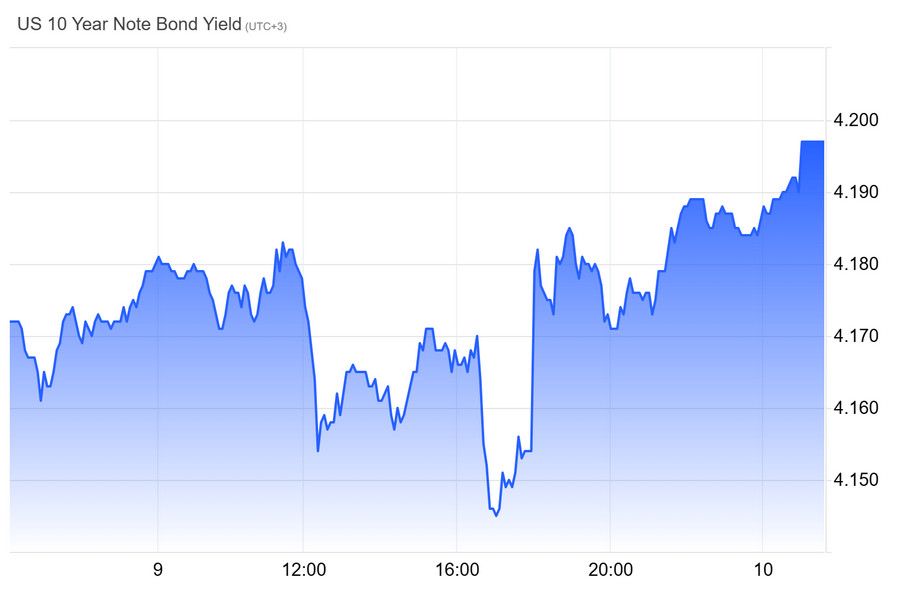

Hartnett believes this combination is risky. A rate cut under a soft stance from the Fed could heighten concerns, leading to increased yields and pressure on stocks. Therefore, attention to Powell's comments and FOMC forecasts is escalating. The bond market also remains tense. The yield on 10-year securities continued to rise, ending one of the weakest weeks in recent months. (Chart 2) Inflation slowed down on Friday, confirming expectations for a rate cut. However, the level of the indicator remains above the target. This casts doubt on the scale of adjustments in 2026. The situation appears excessively active. Even if Hassett takes the helm at the Fed, market participants doubt he will be able to deliver on Trump's ambitions for a rapid cycle of rate cuts.

Kevin Hassett stated that the Federal Reserve has room for a deeper rate cut. He emphasized that upon his appointment as Chairman, he will rely on his own economic judgment, which he claims the President supports. According to Hassett, the evolution of artificial intelligence creates new conditions for monetary policy. A rate cut could expand the aggregate supply and boost demand. During the Wall Street Journal summit, he was asked whether he would support an adjustment exceeding 25 basis points if the data indicated such a possibility. Hassett affirmed that he sees room for such a decision.

This has heightened concerns regarding his dependence on Donald Trump's directives. Moreover, Trump previously stated that rapid changes in borrowing costs would be a criterion for selecting the Fed chief. Hassett stressed that he intends to adhere to his own assessments and dismissed accusations of political dependence. He noted that developing a detailed rate plan six months ahead would be irresponsible. He has previously criticized the Fed for its actions over the past years, considering them politicized. UBS analyst Jonathan Pingle reminded that disagreements over monetary policy are inevitable, and the Chairman's task is to rely on data and explain decisions.

Hassett reported having a good working relationship with Powell. Their contacts remain regular, as in his time working on the Council of Economic Advisers. The new Fed Chairman, appointed by Trump, will take a position on the Board of Governors in January, following the departure of Stephen Miran. In the initial months, he will work under Powell's leadership until his term ends. Hassett believes that, given the anticipated increase in productivity and investments, the potential growth rate of U.S. GDP could be "much higher" than 3%, possibly even exceeding 4%. "There are many opportunities to do something like lowering the interest rate, which will increase the aggregate supply and aggregate demand," he said.

December is traditionally unfavorable for the dollar; however, in the medium term, the divergence in monetary regimes is more important. The Fed is preparing to lower rates, reflecting a slowing economy. The dollar's yield advantage is diminishing compared to the euro and yen. Uncertainty surrounding the future Fed chair, whom the market sees as more dovish, heightens expectations for a prolonged period of low rates. This situation is driving the EUR/USD pair toward the 1.15 level. There is also an alternative scenario.

If the Fed's dot plot indicates a pause and caution, the yield on 2-year Treasury securities may rise. Such a reaction would create short-term pressure on dollar sellers and could trigger a sharp increase in its index. An additional factor is the gap in growth rates. If the U.S. economy maintains a growth rate of around 2% while the Eurozone remains in stagnation, the concept of "American exceptionalism" will continue to support the dollar and limit its correction. Concurrently, the global currency market continues to sell dollars.

According to a survey, nearly 60% of central bank representatives plan to increase the share of assets outside the U.S. dollar. This means they are seeking ways to redistribute reserves and reduce their dollar holdings. However, the greenback's current high liquidity continues to give it an advantage. Meanwhile, the euro is not yet ready to claim the role of a key benchmark. Doubts about the dollar's status this year have intensified due to:

Against this backdrop, some market participants expect a gradual strengthening of positions for the euro and the yuan. However, according to specialists' assessments, the dollar will maintain its central place in the structure of international reserves in the coming years.